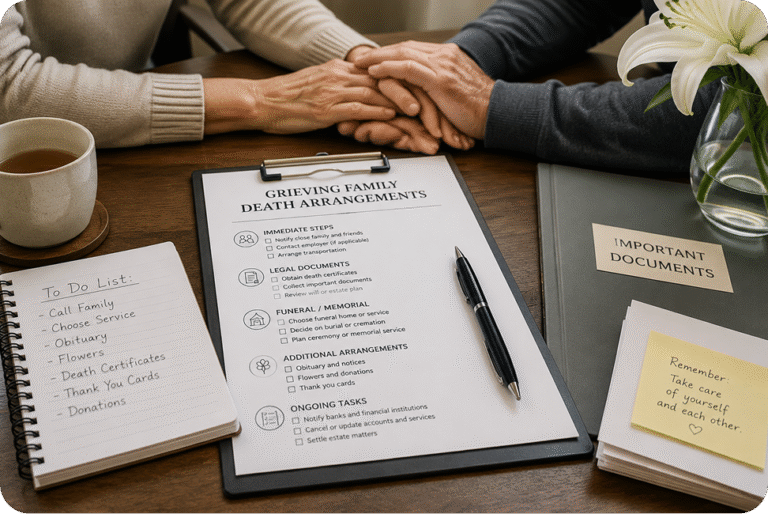

Nobody tells you about the paperwork. You lose someone, and within days you’re staring at a pile of tasks that makes no sense at all. Who do you call first? What documents do you need? Which accounts are even open? Most families have no idea, and that’s completely normal. Nobody prepares for this stuff in advance.

But here’s the thing if you don’t notify the right people after someone passes, it causes real problems. Accounts stay open. Bills keep coming. Identity thieves look for exactly this kind of window. The estate takes a hit, and nobody even realizes it until months later.

A death notification service like Final Closures was set up to handle all of that for grieving families. You tell them what happened once, and their team takes it from there.

You’d Be Surprised How Many Places Need to Know

When most people think about closing accounts after someone dies, they picture maybe three or four places. The bank. Social Security. That’s it.

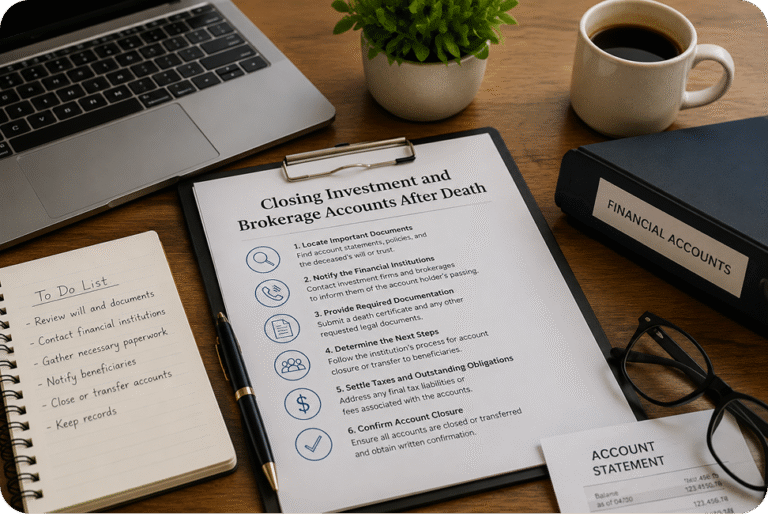

In reality, it’s a lot more than that. The average person today has ties to well over a hundred different organizations. Think about your own life for a second. There’s your bank, but also your credit cards, your phone bill, your streaming subscriptions, your gym membership, your doctor’s office, your insurance company, your email account, your social media profiles, the mortgage company, the IRS, the DMV, any pension or retirement accounts, and on and on.

Each one of those needs to be contacted separately. Each one has its own process. Some want a certified death certificate mailed in. Some have an online form. Some just want a phone call, but then they transfer you three times before anything actually happens.

Doing all of this yourself while you’re grieving is genuinely hard. A lot of families start strong and then just run out of steam somewhere in the middle, which means things get missed.

What Happens When Notifications Don’t Go Out

Missing even a few of these notifications can create headaches that last for years.

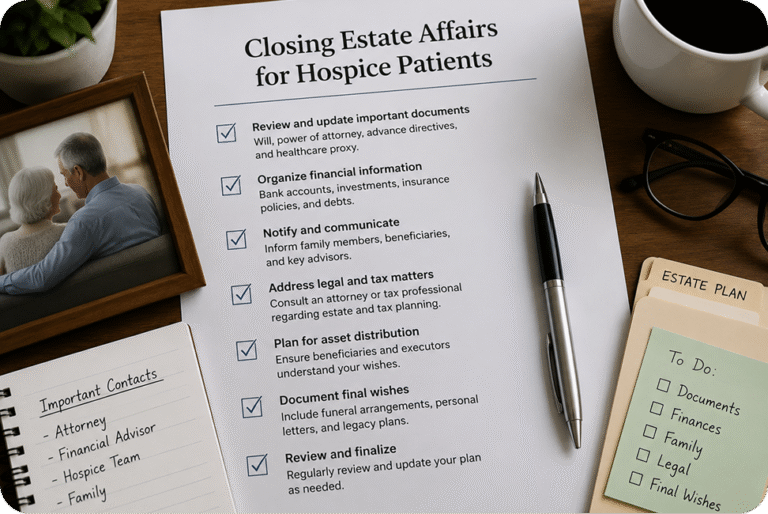

Identity theft is the big one. Fraudsters specifically target deceased people because their credit files stay open until someone shuts them down. It doesn’t take long for someone to open a credit card or take out a loan using a dead person’s name. Every day that passes without notifying the credit bureaus is a day that window stays open.

Then there’s money the family might not know about. Old pension accounts, forgotten bank balances, unclaimed state funds this stuff adds up. A lot of families never collect it simply because they didn’t know to look or didn’t get around to the notification in time.

Subscriptions are another one people overlook. Streaming services, software plans, magazine renewals, cloud storage they all keep charging until someone cancels them. That money comes straight out of the estate and it’s completely avoidable.

And if government agencies like Social Security or the IRS don’t hear from you in time, it creates complications with overpayments and final tax filings that are a pain to unravel later.

What Final Closures Actually Does

The process is pretty simple on your end. You sign up through the Final Closures website and create a secure account. The platform is encrypted so your personal information is protected throughout. Then you pick a plan based on how much coverage you need. Plans start at $399.99 for the basics and go up to $2,399.99 for full coverage across every category.

Once you share the details about your loved one, the Final Closures team handles everything else. They contact each organization the right way, document every notification, and keep track of what’s been done and what’s still pending. You can log in and check the status yourself through a live dashboard so you’re never left guessing.

The basic plan covers the essentials like the credit bureaus, email platforms, and the state DMV. The higher plans bring in pension providers, investment firms, state unclaimed property offices, and everything else.

Why Not Just Handle It Yourself?

You can. Plenty of people try. But most of them end up burning out well before the list is finished.

Part of it is the sheer number of calls. Part of it is the hold times. But honestly, a big part of it is just the emotional weight of explaining what happened to strangers over and over again. Every call to a bank or a government office means retelling the story. That wears on people more than they expect.

Hiring an estate attorney is another option, but attorneys are expensive, and most of this work doesn’t actually need a lawyer. It just needs someone organized and persistent who knows the process. That’s what Final Closures is there for, at a fraction of what an attorney would charge.

They also hold an A+ rating with the Better Business Bureau, so there’s a real track record behind them.

Here’s How You Get Started

Getting set up takes just a few minutes. You go to finalclosures.com, create an account, and enter the basic details about your loved one. From there, the team reviews everything, figures out which organizations need to be notified based on that specific person’s life, and gets to work.

You’ll get updates along the way, and once everything is wrapped up you receive a full summary of what was handled. If anything comes up or you have questions, the team is available to help.

It Makes a Real Difference

The administrative side of losing someone isn’t something most families talk about. But it matters. It protects the estate. It prevents fraud. It keeps money in the family that might otherwise disappear.

More than anything, it saves people from spending months doing something exhausting and unfamiliar at the worst possible time. That’s the whole point of a service like this. You’ve already got enough to deal with. Let someone else handle the calls.