When a loved one passes away, the emotional weight of grief arrives alongside an unexpected avalanche of administrative responsibilities. Among the most pressing concerns for families is understanding the timeline for closing accounts after death and why some accounts take days while others can take well over a year.

There is no single answer. The time it takes depends on the type of account, whether a will exists, the size of the estate, and whether the family has professional help from a Death Notification Service navigating the process. This article breaks down realistic timelines for every major account type and helps you understand what factors can speed up or slow down the entire process.

What Affects the Timeline for Closing Accounts After Death

Before diving into specific timelines, it’s important to understand why there is such a wide range. This is not a single task; it’s dozens of separate processes happening simultaneously across different institutions, each with its own rules, documentation requirements, and internal processing times.

Key factors that influence timelines include:

- Whether the deceased had a will: Estates with a valid will generally move faster through the legal process

- The size and complexity of the estate: Larger estates with multiple assets, properties, or business interests take significantly longer

- Whether accounts have named beneficiaries: Accounts with beneficiaries bypass probate entirely

- The jurisdiction: Probate laws and timelines vary significantly by state

- How quickly families act: Delays in gathering documentation or notifying institutions can add weeks or months

- Whether professional help is involved: Estate attorneys and services like Final Closures can dramatically reduce processing time

What Happens to Bank Accounts When Someone Dies?

This is one of the first questions families ask when closing accounts after death, and the answer depends on the account type.

Solely-owned accounts are frozen or restricted by the bank upon notification of death. The funds become part of the deceased’s estate and must go through the appropriate legal process before they can be distributed. Depending on the state, this may require probate.

Joint accounts with survivorship rights typically transfer automatically to the surviving account holder. The surviving owner usually only needs to present a death certificate to the bank to have the deceased’s name removed.

Accounts with a named beneficiary (also known as POD Payable on Death accounts) transfer directly to the named beneficiary without going through probate. This is one of the fastest account resolution processes, often completed in just a few weeks.

Understanding what happens to bank accounts when someone dies is crucial because banks are often the first institution families contact, and getting this step right early sets the tone for the rest of the estate process.

Account-by-Account Timeline Breakdown

Bank Accounts — 2 to 12 Weeks

For solely-owned accounts, the bank will typically freeze the account upon receiving the death certificate. From there, the timeline depends on whether the estate goes through probate. If the account has a named beneficiary or a small estate affidavit applies, funds can be released in as little as two to four weeks.

How to close a bank account after someone dies:

- Notify the bank and present a certified death certificate

- Identify whether the account has a beneficiary designation

- If no beneficiary, determine whether probate is required

- Present letters testamentary (issued by the probate court) to access and close the account

- Settle any outstanding charges before closing

Credit Cards — 2 to 6 Weeks

Credit card companies should be notified promptly to prevent fraud and stop accruing interest on any outstanding balances. Once notified, they will close the account and provide a final statement. Outstanding balances become the responsibility of the estate, not the surviving family members, unless they were joint account holders.

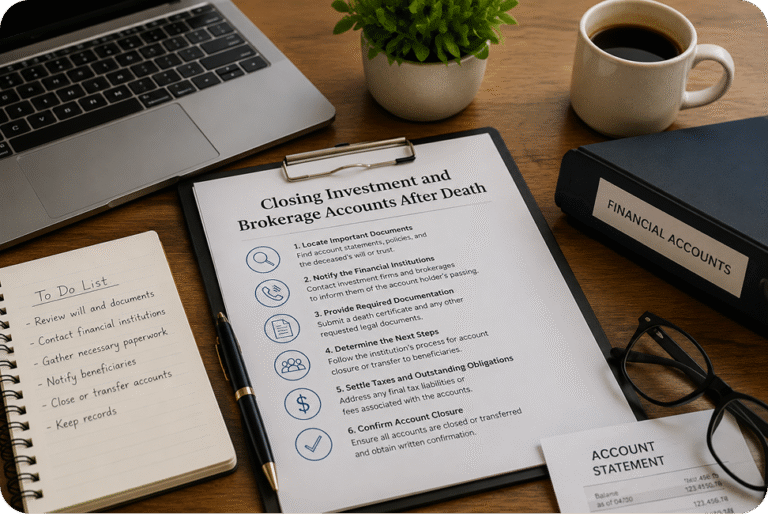

Investment and Brokerage Accounts — 4 to 10 Weeks

These accounts require a death certificate, Letters Testamentary, and potentially a court order before assets can be transferred or liquidated. Accounts with named beneficiaries typically transfer faster, often within four to six weeks. Without a beneficiary, the account enters the estate and may require probate.

Mortgage and Property Loans — 1 to 6 Months

Real estate is among the most complex assets to settle when closing accounts after death. If the deceased was the sole owner, the property enters the estate and must go through probate before it can be sold or transferred. Joint ownership with survivorship rights simplifies the process, but it still requires updating the title and notifying the lender.

Retirement Accounts (401k, IRA, Pension) — 4 to 12 Weeks

Retirement accounts with named beneficiaries bypass probate and can often be transferred within four to eight weeks. Without a beneficiary designation, these accounts become part of the estate and may be subject to a lengthier settlement process. Pension plans vary by employer and may require additional documentation from HR departments.

Life Insurance — 2 to 8 Weeks

Life insurance is one of the faster processes, provided all documentation is in order. Filing a claim with the death certificate and policy information typically results in a payout within two to eight weeks. Delays occur when the policy’s beneficiary information is outdated, disputed, or missing.

Digital and Subscription Accounts — 1 to 4 Weeks

Digital accounts, streaming services, email, social media, and online shopping are among the easiest to close once you have the right information. Most platforms have a dedicated deceased user process and will close accounts within one to four weeks of receiving a request and supporting documentation.

How Long Does Probate Take?

For many families, this is the central question, because probate directly controls when most accounts and assets can be legally distributed.

Probate is the legal process through which a deceased person’s estate is validated and distributed. It is overseen by a probate court and can range from a few months to several years, depending on circumstances.

Typical probate timelines:

| Estate Type | Estimated Probate Duration |

|---|---|

| Small, simple estate | 3 to 6 months |

| Average estate with a will | 6 to 12 months |

| Complex estate (property, business, disputes) | 1 to 3 years |

| Contested will or legal challenges | 2 to 5+ years |

How long does probate take in straightforward cases? Most uncomplicated estates with a valid will move through probate in six to nine months. However, any disputes between heirs, creditor claims, unclear asset ownership, or missing documentation can extend this significantly.

States like California and New York have notoriously lengthy probate processes, while states like Texas offer simplified procedures for qualifying small estates, making the probate timeline one of the most variable parts of closing accounts after death.

What Slows Down the Account Closure Process?

Understanding what causes delays can help families take proactive steps. The most common reasons for extended timelines include:

- Missing or outdated beneficiary designations: One of the single biggest causes of delay

- No will or invalid will: Estates without a will take longer to settle as the court must determine how assets are distributed

- Creditor claims against the estate: Creditors have a legal right to be paid before assets are distributed

- Disputes among heirs: Contested estates can drag on for years in litigation

- International assets: accounts or property held in other countries add jurisdictional complexity

- Delayed death notification: The later institutions are notified, the more complications can arise, including fraud

How to Speed Up the Process

There are several steps families can take to reduce timelines when closing accounts after death:

Act quickly: Notify financial institutions, government agencies, and service providers as soon as possible after obtaining death certificates.

Order enough death certificates: Most institutions require an original certified copy. Order at least 10 to 15 to avoid repeated delays.

Review beneficiary designations in advance: Accounts with up-to-date beneficiary designations bypass probate entirely, saving months of processing time.

Engage an estate attorney early: Legal guidance prevents procedural errors that can cause significant delays down the line.

Seek professional help to manage the process: Rather than contacting each institution individually, a process that can take weeks of phone calls and paperwork, services like Final Closures handle the entire notification and account closure process on your behalf.

How Final Closures Reduce the Timeline

Most families underestimate just how many accounts and institutions need to be contacted. Between banks, credit cards, government agencies, digital accounts, insurance providers, and subscription services, the full list often exceeds 40 separate organisations, each with its own process, documentation requirements, and response time.

Final Closures specializes in managing this entire process efficiently and professionally. By handling notifications simultaneously across all relevant institutions, Final Closures significantly compresses the total timeline, preventing the weeks-long delays that come from families working through each contact one by one while managing grief.

Their team knows exactly what documentation each type of institution requires, which steps can run in parallel, and how to follow up effectively to keep the process moving.

Conclusion

Closing accounts after death is rarely quick, but it doesn’t have to be unnecessarily prolonged. With the right preparation, documentation, and support, families can work through the process efficiently, protecting the estate, preventing fraud, and bringing closure during an incredibly difficult time.

Whether you’re just beginning this process or already partway through, Final Closures is here to help. Visit finalclosures.com to learn how their team can manage your complete account closure process from bank accounts and retirement funds to digital subscriptions and government agencies so your family can focus on healing.

Final Closures is a professional death notification and account closure service, helping families navigate the administrative process that follows the loss of a loved one.