When someone passes away, their finances do not automatically take care of themselves. Bank accounts remain open, direct debits continue, and the money in those accounts cannot be touched by anyone until the proper legal steps are followed. Knowing how to close bank account after death makes the whole process far less confusing and a lot quicker to get through.

Why You Cannot Simply Close Bank Account After Death Yourself

A lot of people assume that because they are a close family member, they can simply go to the bank and close the account. That is not how it works. Banks have strict rules around what happens to a deceased bank account. They cannot just hand over the money to whoever shows up, even if that person is a spouse or an adult child.

The bank needs legal proof that you have the authority to act on behalf of the person who has passed. Without that, they will not release any funds or allow any changes to the account. This is actually there to protect everyone, including the estate and the people who are entitled to what is in it.

The First Thing You Need to Do

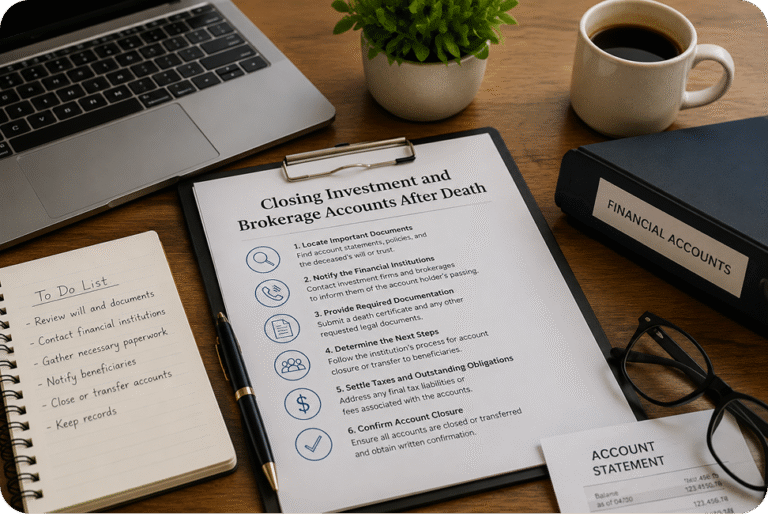

Before you contact the bank, you need to get the death certificate. You will need more than one copy because different institutions will ask for their own. Most families order anywhere from five to ten certified copies, depending on how many accounts and assets need to be dealt with.

Once you have the death certificate, the next step depends on whether the person left a will, whether there is a named beneficiary on the account, or whether the account was held jointly with someone else. Each of these situations is handled differently.

Joint Accounts

If the bank account after death was held jointly, meaning two people were named on the account, the process is usually straightforward. The surviving account holder typically just needs to provide the death certificate to the bank, and the account continues in their name alone.

The bank will update the records and remove the name of the person who has passed. In most cases, this can be done in a single branch visit with the right documentation.

Accounts With a Named Beneficiary

Some accounts have what is called a payable on death or transfer on death designation. This means the account holder named a specific person to receive the funds when they passed. If this is the case, the named beneficiary usually just needs to bring the death certificate and their own identification to the bank. The funds are then released directly to them without going through probate. This is one of the fastest ways to close bank account after death and is significantly simpler than accounts that require full estate administration.

Accounts With No Joint Holder and No Beneficiary

This is where things get a little more involved. If the deceased bank account had no joint holder and no named beneficiary, the account becomes part of the estate. This means it goes through a legal process called probate.

During probate, the court appoints someone, usually called an executor or administrator, to manage the estate. This person is given legal documents, often called letters testamentary or letters of administration, that give them the authority to deal with banks and other institutions on behalf of the estate.

Once you have those documents along with the death certificate, you can approach the bank to begin closing the estate bank account. The bank will verify everything, freeze the account if they have not already done so, and work with the executor to release the funds according to the estate.

What Documents You Will Typically Need

Every bank has slightly different requirements, but most will ask for some combination of the following. A certified copy of the death certificate. A government-issued ID for the person making the request. The legal authority document, such as letters testamentary, letters of administration, or a probate court order. The account details of the deceased, if you have them.

If you are the named executor on a will, having a copy of the will can also be helpful even if the bank does not specifically ask for it. Being prepared with more documentation than needed is always better than showing up without enough.

What Happens to the Money in the Account

Once the bank confirms the authority of the executor or beneficiary, the funds are either transferred or released. When closing estate bank accounts that are part of probate, the money goes into an estate account that the executor manages. From there, it is used to pay any outstanding debts the deceased had, and then what remains is distributed to the beneficiaries named in the will or according to the laws of the state if there was no will. If you are unsure how to close bank account after death and distribute the funds correctly, working with a professional can help you avoid costly mistakes.

If the account had a named beneficiary or was joint, the funds go directly to that person without going through the estate at all.

What to Do If the Bank Account Is Overdrawn

Sometimes a deceased bank account is not in credit. It may have a negative balance or outstanding direct debits still going through. In this situation, the executor will need to deal with those liabilities as part of settling the estate.

You are not personally responsible for the debts of a deceased person unless you were a joint account holder or a guarantor on something. The debts are the responsibility of the estate, not the family members individually.

Stopping Automatic Payments

One of the more practical things to deal with early on is stopping any automatic payments or direct debits going out of the account. These can continue to leave the account even after someone has passed if nobody cancels them.

Contact the bank as soon as possible and ask them to flag the account. Most banks will put a hold on outgoing payments once they are notified of a death, but it helps to be proactive about this. Subscriptions, utility bills, and loan payments can all keep going out if nobody acts quickly.

How Long Does It All Take

Closing a bank account after death can take anywhere from a few days to several months, depending on the situation. A joint account or a payable-on-death account can often be resolved within a week or two. An account going through full probate can take much longer, depending on the complexity of the estate and how busy the probate courts are in your area.

The best thing you can do is start gathering documents early, contact the bank to notify them of the death as soon as possible, and get legal guidance if the estate is large or complicated.

Conclusion

It is not something most people have done before, and it can feel like a lot to figure out at an already difficult time. The key is to take it one step at a time. Get the death certificate, understand what type of account it was, gather the right documents, and then approach the bank with everything in order. Following the right steps to close bank account after death makes the whole process move faster and with far less stress.

If the estate involves multiple accounts, property, or any complexity at all, working with a professional who specializes in final closures can save you a great deal of time, stress, and costly mistakes.