When a loved one passes away, there are a lot of small, quiet tasks that fall on your shoulders during an already difficult time. One of the most important things you can do for them is to protect their financial identity. It is helpful to understand exactly what happens to debt when someone dies so you can take the right steps without feeling overwhelmed. This guide is here to walk you through that process simply and clearly, helping you look after their estate and their name during this tender time.

What Happens to Debt When Someone Dies?

This is one of the first questions families ask, and it deserves a clear answer.

A person’s debts do not disappear after death. They become part of the estate. The estate includes everything the person owned at the time of passing. A legal process called probate determines how those debts get paid. Creditors may file claims against the estate to recover what they are owed.

Most family members are not personally responsible for the debts left behind. That said, if you were a joint account holder or co-signer on any account, some responsibility may still fall on you. An estate attorney can walk you through exactly where you stand.

Why Freezing Credit Matters After a Loss

Just because a person has passed away doesn’t mean their personal details are automatically safe. In fact, identity theft of deceased persons is a very real threat that many families don’t expect. Fraudsters often steal a name or Social Security number to open new credit cards or take out loans, banking on the fact that no one is checking those records anymore. It usually happens quietly behind the scenes, and unfortunately, most families don’t realize there is a problem until the damage is already done.

Freezing your loved one’s credit blocks that door completely. It prevents any new accounts from being opened in their name. It also keeps the estate protected while everything is being settled.

Step-by-Step: How to Freeze a Deceased Person’s Credit

Step 1: Gather the Documents You Will Need

Start by collecting the following:

- Several certified copies of the death certificate

- The deceased’s full legal name, date of birth, and address

- Their Social Security number

You will use these documents at every stage of this process.

Step 2: Contact All Three Credit Bureaus

There are three main credit bureaus in the United States. Each one must be notified separately.

- Equifax: Send a written request along with a copy of the death certificate

- Experian: Mail a letter with proof of your authority, such as an executor status

- TransUnion: Submit a written notice with the required supporting documents

Each bureau will mark the file as deceased. This stops new credit from being issued under your loved one’s name. This step directly addresses what happens to debt when someone dies, from a credit-protection standpoint.

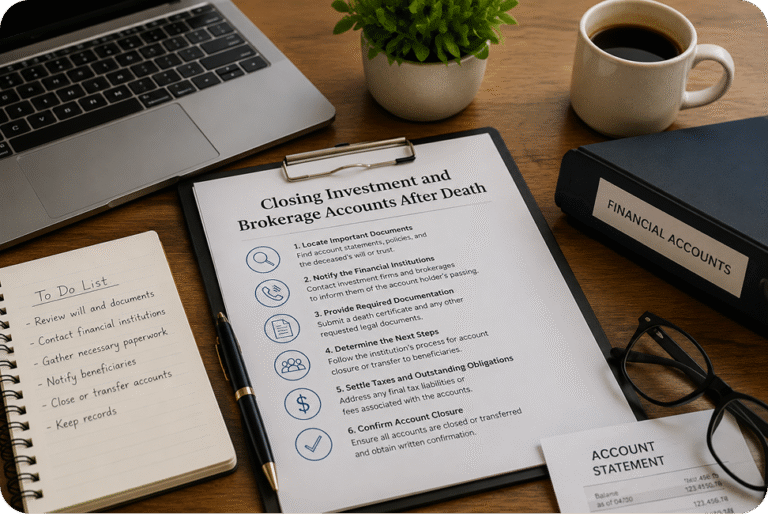

Step 3: How to Close Accounts After Death

Once the credit bureaus are notified, reach out to each bank, credit card company, and lender individually. Ask them to formally close the accounts. Always provide a copy of the death certificate. Keep a written record of every call, including the date and the name of the person you spoke with.

This is also how you cancel accounts after death with utility providers, subscription services, and other recurring billers in the deceased’s name.

Step 4: Notify the Social Security Administration

Report the death to the Social Security Administration. In many cases, the funeral home handles this step. It is still worth confirming that it has been done. This notification flags the Social Security number across financial systems, adding another layer of protection.

A Gentle Reminder About Managing a Loved One’s Finances

Taking these steps is an act of care and protection. You are safeguarding everything your loved one worked for during their lifetime.

Knowing what happens to debt when someone dies helps take away some of the confusion and stress that often follow a loss. There is no need to rush through every single task all at once. It is much better to take each step at a pace that feels okay for you. If you ever run into something that feels complicated or unclear, don’t hesitate to reach out to a professional for a bit of extra help.

You are doing something meaningful during one of life’s most difficult seasons. That effort is not small. It is a final and lasting way to honor the person you love.